A quiet change with loud consequences: the DWP has set out when it can look at your bank data now — and when automated checks could start for millions of claimants next year.

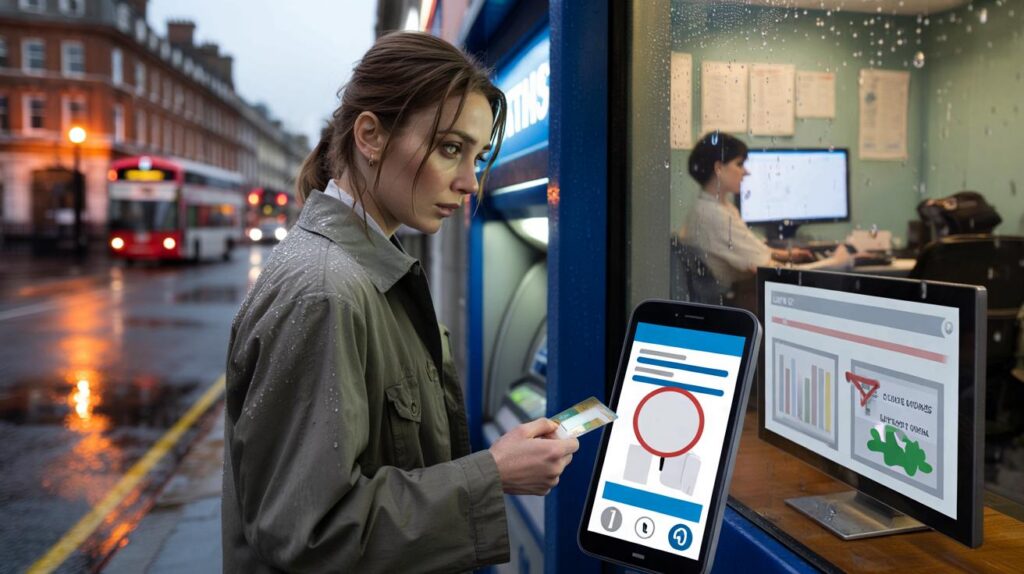

I watched a woman at a cashpoint in Walsall stare at her balance, lips tense, rain soaking the sleeve of her work coat. She checked, rechecked, then tucked her card away like it might snap between her fingers. Somewhere in the background of our lives, tiny decisions around benefits, savings, and side gigs flick on and off like streetlights. You don’t feel them until you do. And when the Department for Work and Pensions says it can check your bank account, suddenly that streetlight feels like a spotlight.

She walked away fast, head down. I wondered if she’d read the same line I had in a policy note this week — the one that spells out exactly when an account can be looked at, and when new bank data sweeps could begin. It’s not paranoia. It’s policy. And the timeline is closer than many think.

When could the DWP look at your account — and what changes next

Right now, the DWP can request information from a bank about a specific person if there’s reasonable suspicion of benefit fraud or error. That covers things like big unexplained deposits, capital above the rules for a means‑tested benefit, or signs someone might be living abroad longer than allowed. It isn’t a fishing expedition. It starts with a case — a tip-off, a mismatch in records, a data ping from HMRC, or an inconsistency in your own claim.

What’s new is the “bank data” power ministers have championed, designed to spot risk without naming you first. Banks would run periodic checks for set markers — for example, balances that look over capital limits for Universal Credit, repeated overseas payments that could suggest a long stay away, or the same account being used for multiple claims. The DWP says this is about flags, not full statements. If a flag triggers, a caseworker can open a targeted inquiry. No green light, no human eyes.

Timing matters. The department has signalled an earliest build-out starting in 2025, with phased rollouts into 2026, subject to Parliament and technical readiness. Until then, nothing changes for most people day to day. **When the system does switch on, it’s expected to focus on means‑tested benefits first — Universal Credit, Pension Credit, Housing Benefit, income‑based JSA and ESA.** Non‑means‑tested benefits and the State Pension aren’t part of routine sweeps, though an individual investigation can still seek bank data if there’s specific suspicion. That’s the line, in black and white.

What actually triggers checks — and how to stay out of the crosshairs

Think of three moments your account is most likely to be checked. First, when you claim or report a change and something doesn’t add up with other records. Second, during a review or “targeted check” where your case falls into a risk pattern the DWP is studying. Third, under the proposed bank data scans, when a bank’s automated search returns a match on a rule: balance apparently over a benefit’s capital limit, frequent foreign transactions over weeks, the same sort code and account number linked to multiple claims. It’s a narrow funnel, not a dragnet.

Here’s a real-world picture. Nadia in Leeds moved onto Universal Credit after losing her job. She’d built £12,800 in savings. UC capital rules allow up to £16,000, but anything over £6,000 reduces your award. A data match spotted the declared savings didn’t reflect a new ISA top-up. She got a message through her journal, sent bank summaries, and her payment was recalculated. No fine, no drama — just a correction. Contrast that with Mark in Portsmouth, whose account showed months abroad while claiming Housing Benefit. Evidence didn’t line up. That became a formal investigation and an overpayment to repay.

So where’s the line? On today’s powers, the DWP needs a reason tied to your case. On the coming bank-data model, banks aren’t handing over everything; they’re returning yes/no signals on set criteria, likely reviewed quarterly or in batches. If your account pings, a caseworker can ask for more. **That means you still have rights: to be told what’s needed, to provide context, to challenge a decision, to seek independent advice.** Bank scanning is the front door; due process should still be the hallway.

Your playbook: tidy facts, clean timelines, calm head

Keep a simple record of savings, payday dates, and any foreign travel that might affect your claim. Take screenshots when you move money between pots, as that can look like new capital. If you live with someone, note who pays what and when, as shared costs sometimes trigger questions about your household status. *A 60-second note in your phone after a change beats an hour of panic later.* Let your benefit journal reflect your real life — even if that life is messy.

Tell the DWP about changes fast: savings crossing a threshold, a new job, a partner moving in, a long stay with family overseas. Silence makes a data flag look suspicious. If you’re asked for statements, send the pages they specify, not a whole shoebox. Let’s be honest: nobody keeps every bank statement in a neat folder. If anxiety spikes, speak to Citizens Advice or a welfare rights worker before you reply. A short, clear timeline of events can turn a knot into a straight line.

There’s a lot of noise around “surveillance.” The reality is more boring — and more navigable.

“Banks aren’t giving the DWP a live feed. They’re answering narrow questions. Most people will never hear a peep unless the numbers tell a convincing story.”

- Means-tested benefits are the focus: Universal Credit, Pension Credit, Housing Benefit, income‑based JSA/ESA.

- Capital limits matter: £16,000 for UC and Housing Benefit; Pension Credit has different savings rules.

- Overseas stays can pause entitlement after four weeks for many benefits — log dates.

- Multiple claims to one account or large unexplained deposits are classic triggers.

- You can challenge decisions and ask for a mandatory reconsideration.

What this means for you — and for how Britain polices benefits

If the new power lands on the 2025–26 timeline the DWP has circulated, it will feel invisible at first. No sirens, just a gradual rise in targeted letters and messages asking for proof. For most claimants, nothing changes unless there’s a mismatch between your story and your statements. For a small minority, the machine will flash red — and a human will step in. The tension is obvious: curb fraud, don’t punish hardship. The test is how carefully those flags are written, and how fairly they’re applied.

We’ve all had that moment where money feels like a test we didn’t study for. The fix isn’t fear. It’s small, boring habits that keep your claim lined up with your bank. If you’re on a means‑tested benefit, know your capital rules and make peace with the admin. If you’re not, bank checks won’t roam your way unless there’s a specific reason. **Some will welcome the crackdown; others will see another layer of cold bureaucracy.** The truth, as usual, sits somewhere between policy notes and people at cashpoints in the rain.

| Key points | Details | Interest for reader |

|---|---|---|

| Current checks | Case-by-case requests when there’s suspicion tied to your claim | Know why you might be contacted today |

| New bank data power | Banks return risk flags on set markers; phased rollout from 2025–26 if approved | Understand what may change and when |

| Who’s in scope | Focus on means‑tested benefits; rights to respond and challenge remain | Gauge your own risk and your options |

FAQ :

- Will the DWP see all my transactions?No. The proposed system asks banks to return flags on set criteria. Detailed statements come later only if a case is opened.

- Does this affect State Pension?Routine bank sweeps target means‑tested benefits. State Pension isn’t means‑tested, though individual investigations can still seek information if there’s specific suspicion.

- What counts as “too much” savings?For Universal Credit and Housing Benefit, capital over £16,000 usually ends entitlement. Between £6,000 and £16,000 reduces awards. Pension Credit has different rules, with tariff income over £10,000 of savings.

- When will the new checks start?The DWP has indicated earliest build through 2025 with staged rollout into 2026, subject to Parliament and technical delivery. Not a big-bang switch-on.

- What should I do if I get a letter?Read it twice, respond by the deadline, and provide the specific pages requested. If unsure, get advice from Citizens Advice or a welfare rights service and keep your reply short and factual.

This reads like classic mission creep: start with “flags” today, full statments tomorrow. You say no green light, no human eyes—but who audits the algorithims? Errors can snowball when banks mis‑match data. Transparency report, please, not just reassurances.